Understanding Credit and Maintaining A Good Score

Your credit score is one of the most important financial factors to impact your life. We have broken down the most significant facets to help you better understand exactly what credit is and how it works, so you can use it to your benefit. It’s never too late to start enhancing your credit score! Let’s begin.

Let’s start by defining some common terminology:

-

Credit: the ability to borrow money with the promise to pay it back with interest

-

Interest: a percentage of the total loan amount paid back to the lender in order to use the money up front

-

Trade Line: listed on a credit report as a record of activity for loans, debts, or lines of credit

-

Installment Loan: a loan with regularly scheduled payments and a final payoff date (such as an auto loan or a personal loan)

-

Revolving Line: a credit line to use, pay down, and use again (credit card, home equity line of credit)

-

Credit Inquiry: a probe of your credit report, which happens when a loan application is completed or a credit report is pulled

What is a Credit Report?

-

A credit report is a detailed breakdown of previous and current credit responsibilities which are reported by a credit bureau.

-

The three most commonly used credit bureaus are Experian, Equifax, and TransUnion.

What is on a Credit Report?

-

Name, address, DOB, employment, and social security number

-

Any type of loan, along with real estate, credit cards, and lines of credit

-

Collections or public records (such as bankruptcy and charge-offs)

-

Credit inquiries in the past 2 years (source, type, and date of inquiry)

What is a Credit Score (also known as FICO Score)?

-

FICO (Fair Isaac Company) is a three-digit number that is determined by the weight of five score factors:

-

35% Payment History - timeliness of payments, with more weight on the last two years

-

30% Total Balances/Amount Owed - balances owed on trade lines and the amount of credit available on revolving lines

-

15% Length of Credit History - Average length of credit on all trade lines

-

10% Mix of Credit - Types of trade lines (real estate, installments, and revolving lines of credit)

-

10% New Credit - Accumulation of new debts and inquiries

-

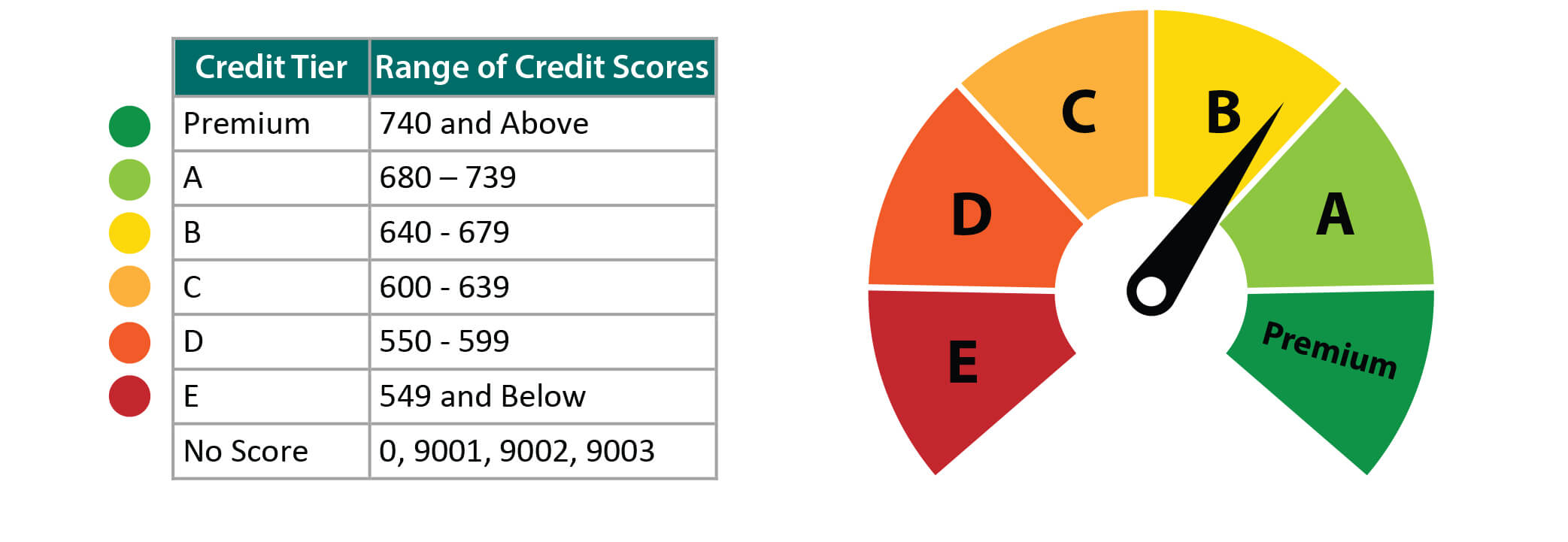

A score can be as low as 300 and as high as 850. If you have never used your credit before, you will not have a score.

Every score fits into a credit tier with “Premium” being excellent credit and “E” being credit with opportunity to improve. Once you know what goes into calculating your score, you can always work to improve it, if needed. It is not a set number. If your financial habits change, your score will too.

How do you get a Credit Score?

What is Fragile Credit?

-

If a person does not have much credit history, they might be considered fragile.

-

Fragile credit is not necessarily bad credit. It simply means one does not have a lot of credit experience.

What are some actions to avoid that can cause damage to a Credit Score?

-

Missed or late payments

-

Credit cards that are maxed out or near capacity

-

Excessively applying for loans, credit cards, or lines of credit (including inquiries)

-

Opening numerous trade lines in a short period of time

-

Lacking a healthy mix of trade line types (such as installments, revolving lines, and real estate)

-

Open collections or charged off trade lines

How can you boost your Credit Score?

-

Making consistent and on-time payments

-

Paying down revolving lines of credit

-

Refinancing revolving debt into installment debt

-

Slowing down on taking out loans

-

Paying off collections and charged off trade lines

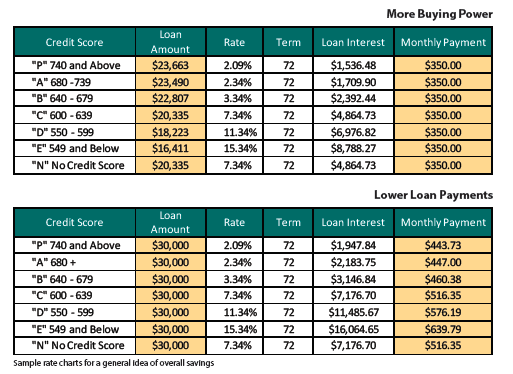

Why is it so important to maintain a good Credit Score?

-

Higher chance of credit approval. A positive credit history shows lenders that you are less of a risk to lend to.

-

Lower interest rates. Paying less interest on your debt will save money over time.

-

Lower payments

-

Approval for higher limits on credit cards

-

Easier borrowing in the event of an emergency or last-minute decision

Overall, being “credit smart” means you can save more money, be able to buy larger purchases easier, make emergencies less financially stressful, and pay off debts faster.

You can download a PDF overview of this information for your convenience and records.

Live Smarter

If you have any questions, or would like to dig deeper into your personal credit, we’re happy to help. Give us a call at 315-735-8571 to talk about your options or make an appointment with one of our friendly Member Service Representatives today. Simply click on the button below, select “Advisory Services” from the menu, and choose “Financial Checkup”.

Bring This Session to a Live Setting

If you would like to schedule our Community Educator for a seminar or workshop for any Financial Friday educational topic, please email your request to FinancialEducation@fsource.org

Interested in learning more? There are also additional resources which have been created specifically to help you best control and leverage your finances. Feel free to use these anytime!